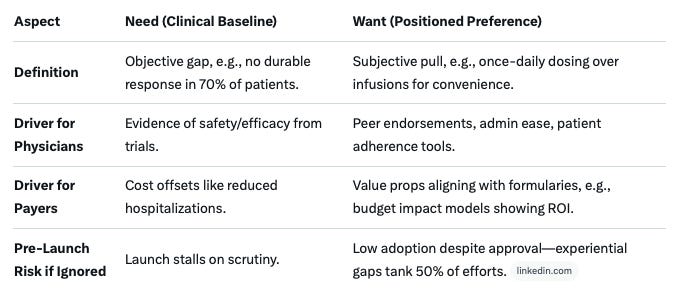

Unmet Need is Not Fixed

Positioning Wants in Pharma’s Pre-Launch Landscape

In the world of pharmaceutical launches, “unmet need” is often treated like, and talked about as, an unchangeable North Star - a clinical void so glaring that any therapy filling it should sail to blockbuster status. But the uncomfortable truth is that unmet need isn’t fixed. It’s a shiftable narrative, a perception, and a construct that pharma companies can - and must - reposition long before approval.

Take GSK’s Arexvy, the RSV vaccine that captured 70% market share in its debut year, racking up $1.5 billion in sales despite a crowded field. Its edge? Pre-launch positioning that didn’t just highlight the clinical gap in older adult protection but framed it as an urgent, preventable crisis with seamless integration into primary care workflows. I bet you’ve heard about RSV recently? That’s not an accident, or an ‘ask’ by the medical community.

This isn’t luck; it’s strategic positioning at work - creating an ideal landing pod for the right craft. Traditional launches chase static needs, like superior ‘efficacy’ in oncology (remember, there’s no such thing as ‘efficacy’). But in 2025’s post-IRA landscape, where payers ration every dollar and physicians juggle burnout with evidence overload, success pivots on repositioning “wants” - subjective desires for convenience, support, and alignment that drive 40% of physicians’ brand preferences beyond pure clinical data. Needs are the objective baseline: a therapy that extends progression-free survival. Wants? The once-monthly infusion that frees up a clinic’s schedule, or the real-world evidence package that sways a formulary committee.

I wanted to unpack the want-vs.-need dichotomy, explore pre-launch tactics to position physicians’ and payers’ preferences, and dissect real-world wins.

I suspect, for this blog, the question isn’t if you can reposition the market - it’s how to do it before competitors even notice the gap.

Want vs. Need: The Positioning Pivot in Pharma Decision-Making

Picture a hematologist facing a relapsed multiple myeloma patient. The “need” is clear: a regimen with better durability than standards. But the “want”? A therapy positioned as minimizing site-of-care disruptions, backed by peer-validated data, and bundled with patient navigation tools to boost adherence.

Ignore the wants, and even gold-standard efficacy underwhelms - 50% of launches underperform due to experiential mismatches, not trial failures. Needs are data anchors: endpoints from Phase 3 proving safety and superiority. Wants are behavioral magnets: preferences honed by workflow realities, economic pressures, and ecosystem enablers. As (even) Deloitte’s 2025 commercial outlook notes, biopharma must “reimagine engagement” in an agile, tech-infused era where stakeholder perceptions shift quarterly. (I say ‘even’ because Deloitte markets like an accountant…) Unmet need feels etched in stone in regulatory filings, but it’s malleable - repositioned by real-world evidence, stakeholder dialogues, and narrative reframing. Regulators are human too, influenced by stories, and constructs, without realising that they are.

In low-unmet-need arenas like generics-saturated hypertension, pharma amplifies wants through targeted education, effectively “creating” perceived gaps via sharp positioning. Patients underscore this: Recent surveys show only about half feel pharma truly addresses their holistic needs, with affordability and access tipping loyalty scales. As Philip Kotler put it: “Marketing is the science of satisfying needs and wants through an exchange process.” But in 2025, with AI-driven personalization and RWE exploding, the exchange starts pre-launch - and deep positioning is the lever.

To visualize the pivot:

This framework isn’t abstract; it’s a positioning blueprint that turns fluid perceptions into launch velocity.

Positioning Physicians’ Wants: From Skeptics to Advocates

Physicians aren’t passive recipients of data - they’re time-strapped decision-makers whose brand appetite comes from non-clinical enablers like robust support and simplicity. Pre-launch is the window to reposition skepticism into advocacy, co-crafting narratives that make your asset indispensable. Even in the ZS (who tend not to grasp the idea of positioning at all) 2024 trends report, they emphasize that in a fragmented ecosystem, early experiential hooks outpace late-stage blitzes.

Tactics to Deploy 18–24 Months Out:

KOL/HCP Co-Creation: Launch advisory boards and VR simulations to mine pain points, evolving your story collaboratively. This boosts advocacy by 20–30%, as HCPs become co-authors on publications on subgroup unmet needs. Track via Net Promoter Scores - top launches engage 2x more providers pre-approval.

Educational Momentum: Deploy webinars, CMEs, and whitepapers reframing paradigms: “Your toolkit misses X% of high-risk cases - evolve with us.” Digital personalization via AI nudges fosters pre-launch excitement, per IQVIA’s 2025 playbook.

Experience Differentiation: Prioritize wants like ease of dosing. Bayer’s Xarelto nailed this with ‘once-daily convenience’, seizing 50% share post-launch despite equivalent efficacy. Pair with apps for adherence tracking to reduce admin loads.

Feedback Micro-Loops: Assemble cross-functional “battle teams” for iterative HCP input, honing messaging to fuse needs with wants.

A quick takeaway from recent polls: 70% of physicians prioritize medical information at diagnosis but won’t ignore peer networks for validation - lean into hybrid forums to bridge that gap. In the shadow of their reported burnout, these touches don’t just inform; they empower - and position your brand as the thoughtful partner.

Influencing Payers’ Wants: Securing Access Before Day One

Payers greenlight just 30% of new drugs in Year 1, denying over 70% for chronic conditions amid IRA squeezes - pre-launch positioning is a counterpunch, proving value that fits their playbook. Shift from “add-on risk” to “portfolio essential” by tailoring economics early.

Proven Plays, 6–18 Months Pre-Approval:

Data Exchanges Under Cures Act: Share MOAs, trials, and budget models proactively. Highlight hospitalization reductions for ROI alignment - Simon-Kucher’s 2025 trends flag RWE as a payer “want” for JCA compliance.

Segmented Value Stories: Customize for PBMs vs. plans: “Ditch legacy spend on X for Y outcomes.” HEOR dossiers justify premiums in oncology, per TJPA’s access pillars.

Archetype Targeting: In rare diseases, educate on burden via patient voices; in generics fields, pitch off-label prevention. Engage via ICER forums to influence guidelines.

Outcome-Based Contracts: Tie rebates to real metrics, quelling accountability fears in an IRA world.

Early engagement lifts formulary odds by 25%, per 2025 access reports - a real metric for success. As one payer exec quipped: “We want ‘spend on X buys Y’ - deliver it pre-filing.”

Case Studies: Proof in the Pipeline

Theory shines in practice. Here’s how deep positioning turned needs into wants:

Celgene’s Revlimid: A “drumbeat” of pre-launch evidence - twice as much as rivals’ studies - kept hematologists involved with evolving data, sustaining myeloma dominance despite generics looming.

2018 Migraine Disruptor (Aimovig): Unbranded DTC via advocacy coalitions and PR built patient demand, reframing under-diagnosis as an “evolving crisis” - scripts surged 30% at launch, influencing HCPs and payers alike.

Rare Disease Reimbursement Win: Early payer “burden-of-illness” dialogues with patient input secured rapid access, transforming niche needs into budgeted wants via frameworks like PPEF.

These aren’t outliers - first-to-market loses if the wants lag.

The Positioning Playbook: Act on Fluid Needs Now

Unmet need isn’t destiny - it’s the dough you knead into wants via KOL co-creation for HCPs and HEOR tales for payers. In 2025’s competitive landscape, pre-launch positioning isn’t a nice-to-have; it’s your moat - aligning seamlessly with the deep positioning principles we’re unpacking here.

Expanding on the Five Rules of Pharmaceutical Positioning: A Deeper Dive for Strategic Minds

In the ever-evolving arena of pharmaceutical launches, where unmet needs morph into shaped wants and clinical data battles payer scrutiny, my Five Rules of Pharmaceutical Positioning are a guide for those crafting not just products, but market shifts. As outlined in the Substack post, these rules distill the essence of “Deep Positioning” - a proactive, product-centric approach that embeds differentiation from the lab bench to the formulary.

While the original framework captures the high-level imperatives, let’s expand on each rule here, weaving in practical implications, real-world pharma examples and my own case studies, and ties to today’s post-IRA pressures. This isn’t theory; it’s a playbook for turning fluid perceptions into fortified market strongholds.

Drawing from my nine principles in Pharmaceutical Positioning, these five rules emphasize early, intentional action. Deep positioning challenges the inertia of “the obvious path” in R&D, urging teams to position not as an afterthought, but as the North Star guiding every decision. Let’s look, rule by rule.

Rule 1: Deep Positioning is About the Product

At its core, this rule flips the script on superficial brand-building. Traditional positioning - glossy ads etching a “lifestyle” image into HCP minds - treats the drug as a canvas for marketing flair. Deep Positioning is more surgical: a relentless focus on the molecule’s intrinsic and extrinsic architecture: indication selection, dosing regimens, formulation tweaks, endpoint choices, and the value proposition forged in Phase I/II. The drug’s DNA doesn’t change post-discovery; what evolves is how you sculpt it into a differentiated contender.

Expansion and Application: In a world where 70% of launches underperform due to commoditized perceptions, this rule demands baking in “unmet need evolution” from day one. Consider Novartis’ Entresto in heart failure: Early decisions to prioritize sacubitril/valsartan’s unique dual mechanism (neprilysin inhibition + ARB) over generic ARBs created a product inherently positioned as a “paradigm shift,” not just another add-on. (I know, because Entresto was regarded as a prerequisite in my regimen, even in the UK’s NHS…)

This wasn’t marketing spin; it was endpoint design yielding ARNI superiority data that payers couldn’t ignore, driving $5B+ peak sales. I worked on Entresto, repositioning it in the US, after an underwhelming launch - we focused on talking to payers, and that traction from the development programme took off…

For your pipeline: Audit early development milestones. Ask: Does this formulation address a “want,” such as oral over IV, for community settings? Tie it to Rule 3’s future vision - position the product to become the convenience king, evidenced by adherence studies in the trials. In low-unmet-need spaces like hypertension/ heart failure, this granular focus turns generics parity into premium wants, like once-weekly dosing that slashes clinic visits by 50%.

Rule 2: The Best Time to Position Your Drug Was in Phase I. The Next Best Time is Now.

Timing isn’t a luxury; it’s the difference between optionality and regret. Phase I/II choices - target effect size, comparator arms, even preliminary value props - lock in (or sabotage) your trajectory. Delay, and you’re handcuffed: Clinical teams chase easy, precedented endpoints, regulatory filings balloon, and market access hits walls built by indecision. My rule is a wake-up for those who want a good day: Engage Deep Positioning early to inject strategic oxygen, preserving flexibility amid market flux.

Expansion and Application: Pharma’s “valley of death” isn’t funding - it’s the positioning void between discovery and proof-of-concept. GSK’s Arexvy RSV vaccine exemplifies this: Phase I insights into older adults’ wants (e.g., single-dose simplicity) informed antibody persistence endpoints, yielding data that positioned it as the “preventive essential” pre-launch, gaining 70% share despite rivals. Contrast with delayed entrants like Moderna’s mRESVIA, which trailed due to later pivots.

Practically: Form cross-functional “positioning pods” in Phase I - R&D, commercial, HEOR working together and debating: “What effect size unlocks payer ROI?” This echoes my “Unmet Need is Not Fixed” thesis: Shape wants via early HCP advisory boards, quantifying how your asset evolves clinical paradigms. In 2025’s IRA era, where negotiations start 18 months pre-launch, this rule buys you the agility to adapt to HTA shifts, potentially lifting formulary odds by 25%.

Rule 3: Write ‘…Will Become’ at the Top of the Positioning, Not ‘Is’.

Static positioning statements - ”Our drug is a potent inhibitor” - are graveyards for ambition. My rule ignites foresight: Frame as “Our drug will become the first-line option for high-risk subgroups, backed by RWE on adherence gains.” This aspirational anchor isn’t a nice-to-have; it’s a directive, pulling teams toward evidence generation that realizes the vision. It transforms positioning from a descriptive echo chamber into a prophetic engine.

Expansion and Application: In physician decision-making, where 40% of preferences hinge on experiential “wants,” this future tense fosters narrative momentum. Eli Lilly’s Mounjaro (tirzepatide) mastered it: Early positioning as “the dual GIP/GLP-1 that will become the obesity standard” drove endpoint expansions into weight loss, evolving from diabetes “need” to blockbuster obesity want. Result? $5B sales in Year 1, reshaping markets.

For implementation: Draft a “will become” North Star in a one-page manifesto, shared quarterly. Link to KOL co-creation - envision subgroup benefits, then design trials (even pII trials) to prove them. This aligns with payer tactics: Pre-approval HEOR models project “will become” budget impacts, preempting denials. In saturated fields, it “creates” unmet need, like reframing statins as “will become” CVD preventives with novel biomarkers.

Rule 4: Find Your ‘Mechanism of Value’

Benefits are table stakes; value is the moat. This rule probes deeper than efficacy platitudes (”reduces A1c”) to the “why” that resonates: the Mechanism of Value (MoV) - that unique clinical-economic hook tying lab outcomes to stakeholder wins. It’s not a vague benefit ladder; it’s quantified proof of worth, demanding you dissect granular outcomes (e.g., “avoids 2 hospitalizations per 100 patients”) over abstract claims.

Expansion and Application: Payers reject 70% of new chronic therapies in Year 1 - MoV flips that by bridging academic discovery to real-world ROI. Pfizer’s Paxlovid hit it perfectly: MoV as “oral antiviral that accelerates recovery by 89%, slashing hospital burden“ wasn’t just antiviral potency; it was cost-offset mathematics for overwhelmed systems during COVID. This positioned it as indispensable, securing emergency access.

To operationalize: Map MoV via patient journey audits - identify “wants” like reduced caregiver time, then endpoint them (e.g., QALY gains). In oncology, it’s subgroup MoVs: “Will become the maintenance therapy extending PFS by 6 months in BRCA+.” Tools like budget impact models quantify it early, per Simon-Kucher benchmarks, ensuring your positioning withstands ICER scrutiny. You can easily see why this is a phase I/ phase II exercise - leaving these value endpoint explorations for phase III is too late.

Rule 5: Don’t Allow People to Position Your Drug Who Don’t Realise They’re Doing So

“Positioning by accident” is pharma’s silent killer: indication picks, sci-comm or medical affairs platforms, even brand names, set de facto frames of reference. My rule demands vigilance: Every market-shaping choice must be intentional, lest passive decisions (e.g., a narrow label) box you into commoditization.

Expansion and Application: Pseudo-positioning plagues 50% of underperformers - think drugs named for mechanisms (e.g., “Janus Kinase Inhibitor X”) that shout “me-too.” Amgen’s Prolia dodged this: Conscious early framing as “anti-sclerostin for bone health evolution” avoided osteoporosis generics traps, positioning as the “architectural” builder with $4B peaks.

Guardrails: Embed positioning reviews in governance - veto naming that hints at parity; evolve scientific platforms to “future-proof” narratives. Tie to HCP engagement: Unwitting KOL quotes can cement weak framings; curate them to amplify MoV. In payer plays, this means pre-filing dialogues framing your asset as “portfolio optimizer,” not “incremental cost.”

Additional Illustration: Bristol Myers Squibb’s Reblozyl (Luspatercept) – Pioneering EMAs to Upend Anemia’s ESA Monopoly

One of my favourites, because we were at the core of this…

In the transfusion-dependent anemia landscape - long beholden to erythropoiesis-stimulating agents (ESAs) like Amgen’s Epogen, which propped up early red blood cell progenitors but often fell short on durable responses - BMS revolutionaries at Acceleron challenged the foundational definition of “stimulation.” What if efficacy wasn’t about kickstarting production but maturing late-stage erythroblasts? This probe gave rise to Reblozyl, the first-in-class erythropoiesis maturation agent (EMA), approved in 2019 for beta-thalassemia and expanded in 2023 to myelodysplastic syndromes (MDS).

By reframing anemia treatment from “ESA stimulation” (with risks like tumor progression signals) to “EMA maturation” - evidenced by MEDALIST and BELIEVE trials showing 30–40% transfusion independence rates - Reblozyl didn’t just compete; it redefined the paradigm. Pre-launch KOL collaborations unpacked “unmet need” into dimensions like QoL beyond hemoglobin thresholds, while HEOR models quantified outlier ROI in ring sideroblasts+ MDS subsets.

The effect? ESAs’ market share eroded by 15–20% in key indications by 2025, with Reblozyl hitting $1B+ sales and inspiring follow-ons like Merck’s bomedemstat. This definitional change commoditized a $5B ESA duopoly, proving my rule: Interrogate terms like “anemia therapy,” and opportunity floods in - turning a niche biologic into a category creator.

Positioning as Your Revolutionary Edge

My five rules aren’t checkboxes; they’re a manifesto for pharma revolutionaries, echoing my “Rules for Pharma Revolutionaries” ethos of bold, early bets. In an era where wants eclipse fixed needs, they empower you to sculpt markets proactively - turning Phase I hunches into launch moats. The molecule doesn’t change; your decisions do.